Unexpected financial crises can strike at any moment. Whether it’s a medical emergency, a sudden car repair, or an unexpected job loss, such emergencies can throw a wrench in your carefully planned budget. In times like these, having access to quick financial support can make all the difference. Personal emergency loans are one of the most reliable ways to get the money you need when you’re facing an unforeseen situation.

Personal emergency loans provide fast access to funds with the flexibility to use them for a variety of urgent needs. This article explores the various aspects of personal emergency loans, including how they work, the different types available, the advantages, and the factors you should consider before applying for one.

What Are Personal Emergency Loans?

Personal emergency loans are unsecured loans offered by banks, credit unions, and online lenders to help individuals meet urgent financial needs. The loan amount can vary depending on the lender, and in most cases, the money is provided as a lump sum, which the borrower must repay over a specified period with interest.

Unlike a traditional loan, which might be intended for specific purposes like home improvement or auto financing, an emergency loan can be used for anything related to the emergency. This could include medical bills, car repairs, emergency travel, or even paying rent to avoid eviction.

These loans are typically short-term and come with relatively higher interest rates than other types of personal loans due to their urgent nature. However, the appeal of personal emergency loans is that they provide fast access to funds when other forms of credit might not be available.

Interest Rates for FIRSTmoney Emergency Loans

| Types of fees | Applicable charges |

| Emergency loan interest rate | Starting at 10.99% |

| Processing fees | Processing fees of up to 2% will be deducted from the loan amount at the time of disbursal |

| Late payment fees | 2% of the unpaid EMI |

| Stamping charges | As per actuals |

| Foreclosure charges | Nil |

| EMI bounce charges | ₹500 |

| Cheque or mandate swap charges | ₹500 |

| EMI pickup or collection charges | ₹500 |

| Physical statement of account / Repayment schedule | ₹50 |

How Do Personal Emergency Loans Work?

Personal emergency loans typically work by providing a lump sum of money that you borrow from a lender. Once approved, the lender deposits the loan amount into your account or issues a check for you. You then repay the loan in installments over a period, which can range from a few months to several years, depending on the loan terms.

The loan’s repayment terms include:

- Loan Amount: The total sum of money borrowed, which can vary from a few hundred to several thousand dollars.

- Interest Rate: The percentage charged on the loan amount, often higher for emergency loans than other types of personal loans.

- Repayment Period: The period over which the loan is repaid, which could range from 3 to 60 months or more.

- Fees: Some loans may come with origination fees, late payment fees, or other charges.

Once the loan is disbursed, the borrower is responsible for making regular payments, which typically include both the principal and the interest.

Pros and Cons of Personal Emergency Loans

Pros:

- Fast Access to Funds: Emergency loans are designed to provide quick access to funds, helping you address immediate financial needs without delay.

- Flexibility: These loans can be used for various purposes, such as medical emergencies, home repairs, and car repairs.

- No Collateral Required: Most emergency loans are unsecured, meaning you don’t have to provide assets as collateral.

- Improved Credit: If you have a strong repayment history, taking out an emergency loan and paying it off on time can help improve your credit score.

Cons:

- High-Interest Rates: Emergency loans tend to come with higher interest rates compared to standard personal loans.

- Risk of Debt: If you fail to repay the loan, you may incur late fees, higher interest charges, and damage to your credit score.

- Short-Term Nature: These loans typically have shorter repayment terms, which means you may have higher monthly payments.

- Qualification Requirements: Some lenders may require a minimum credit score or proof of income, making it difficult for some people to qualify.

How to Qualify for a Personal Emergency Loan

Qualification requirements for personal emergency loans can vary depending on the lender and the type of loan. However, most lenders will look at the following factors when determining whether or not you qualify:

- Credit Score: Lenders often consider your credit score to assess your ability to repay the loan. A higher score typically increases your chances of qualifying for a loan.

- Income: Lenders will ask for proof of income to ensure you have the financial means to repay the loan.

- Debt-to-Income Ratio: Lenders may look at your debt-to-income ratio to ensure that your existing debts do not prevent you from repaying the new loan.

- Employment Status: A stable job history or employment status is often required for personal emergency loans.

Types of Personal Emergency Loans

Personal emergency loans come in various forms, each with its own advantages, disadvantages, and specific use cases. The choice of loan depends on factors like the amount of money needed, the speed of disbursement, your creditworthiness, and the urgency of your situation. Below are the main types of personal emergency loans that can help you handle unexpected financial crises:

1. Traditional Personal Loans

Traditional personal loans are unsecured loans provided by banks, credit unions, and other lending institutions. They are one of the most common options for borrowers in need of emergency funds, offering fixed loan amounts, repayment terms, and interest rates.

- How It Works: You can borrow a lump sum of money, which you must repay in monthly installments over a set period (usually 1 to 5 years). The interest rate is generally fixed, and you may qualify for a personal loan if you have a decent credit score and a stable income.

- Pros:

- Lower interest rates compared to other emergency loan types.

- Fixed repayment terms, making budgeting easier.

- Larger loan amounts, allowing you to cover significant expenses.

- No collateral required, as most personal loans are unsecured.

- Cons:

- Longer approval and funding time, especially if applying through a traditional bank.

- A good to excellent credit score is often required to secure favorable terms.

- Late payments can lead to significant fees and negatively impact your credit score.

2. Payday Loans

Payday loans are small, short-term loans designed to cover emergency expenses until your next paycheck arrives. These loans typically come with high interest rates and fees, making them a quick but expensive solution for short-term financial crises.

- How It Works: The loan amount usually ranges from $100 to $1,000, and you repay it in full on your next payday, typically within two weeks to a month. The lender may require access to your bank account or post-dated checks to secure the loan.

- Pros:

- Extremely fast approval process, often within minutes.

- No credit check required, making them accessible to individuals with bad credit.

- Can be applied for and received online, making them convenient for those in urgent need.

- Cons:

- Extremely high-interest rates and fees that can make the loan significantly more expensive.

- If you are unable to repay the loan on time, it can lead to a cycle of debt with additional fees and interest charges.

- The short repayment window can be difficult to manage for borrowers with tight finances.

3. Online Emergency Loans

Online emergency loans have gained popularity in recent years, especially for individuals who need money quickly and may not qualify for traditional loans. These loans are offered by online lenders, and the entire application and approval process is typically done digitally.

- How It Works: The process for securing an online emergency loan is simple and can be completed entirely online. After submitting your application, the lender assesses your eligibility, and if approved, funds are usually disbursed within one to two business days. Online lenders may offer both unsecured personal loans and payday loans, depending on the amount requested.

- Pros:

- Fast approval and disbursement, often within 24-48 hours.

- Fewer qualification requirements compared to traditional lenders (some lenders accept borrowers with poor credit).

- No need to visit a bank branch; everything is handled online.

- Flexible loan amounts ranging from small loans to larger amounts.

- Cons:

- Interest rates can be higher than traditional personal loans, especially if you are borrowing a smaller amount or have bad credit.

- Some online lenders may charge hidden fees, such as processing fees or late payment penalties.

- The online loan market is rife with unregulated lenders, so there is a risk of encountering scams.

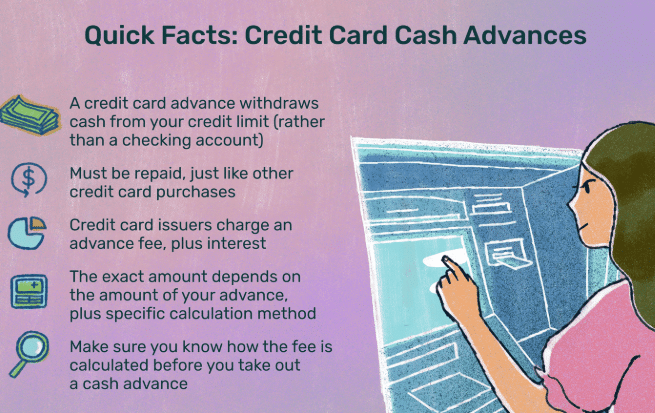

4. Credit Card Cash Advances

A credit card cash advance is another form of borrowing money quickly in times of emergency. If you have available credit on your credit card, you can withdraw a certain amount of cash (often at an ATM or bank) and repay it with interest.

- How It Works: Credit card issuers allow you to access a portion of your credit limit in cash. You will be charged a cash advance fee (typically a percentage of the amount withdrawn) and high-interest rates, which begin accruing immediately after the withdrawal. Repayment is required according to your credit card’s terms, and cash advances are typically not eligible for an interest-free grace period.

- Pros:

- Quick access to cash, especially if you already have a credit card with an available balance.

- No need for a formal loan application process or approval—if you have the credit limit, you can withdraw the money.

- Cons:

- High-interest rates and fees make cash advances a very expensive option.

- No grace period, so interest begins accumulating immediately.

- Cash advances often have lower limits than regular credit card purchases, meaning they may not be suitable for larger emergencies.

5. Home Equity Loans and Lines of Credit (HELOC)

A home equity loan or a HELOC allows you to borrow against the equity in your home. These loans are typically offered at lower interest rates compared to unsecured personal loans or payday loans because they are secured by the value of your property.

- How It Works: With a home equity loan, you borrow a lump sum of money based on the value of your home and repay it over a set term. Alternatively, a HELOC functions like a credit card, allowing you to borrow up to a certain limit and only pay interest on what you use.

- Pros:

- Lower interest rates compared to unsecured loans due to the collateral of your home.

- Larger loan amounts, making them ideal for covering significant emergency expenses (e.g., major medical bills or home repairs).

- Long repayment terms make it easier to manage payments.

- Cons:

- Your home serves as collateral, meaning failure to repay the loan could result in foreclosure.

- The application process can take longer, as the lender needs to assess your property’s value.

- Not ideal for renters, as they don’t own the home and cannot use it as collateral.

6. Auto Title Loans

Auto title loans allow you to borrow money using your vehicle’s title as collateral. These loans are similar to payday loans in that they provide quick access to cash but come with the risk of losing your vehicle if you cannot repay the loan.

- How It Works: To obtain an auto title loan, you need to own your vehicle outright (or have significant equity in it). The lender places a lien on your car’s title, and if you fail to repay the loan, they have the right to repossess your vehicle.

- Pros:

- Quick approval process, often within a few hours.

- No credit check is required, making them accessible to individuals with poor credit.

- You can continue to use your car while repaying the loan (though it is collateralized).

- Cons:

- High-interest rates and fees, making the loan quite expensive.

- If you fail to repay the loan, the lender may repossess your car.

- Only a small amount can be borrowed based on the car’s value.

7. Family and Friend Loans

While not a formal type of loan, borrowing money from family or friends can be a solution in an emergency. This type of loan doesn’t typically involve interest or fees, but it can strain personal relationships.

- How It Works: You ask a close family member or friend to lend you money for an emergency. Repayment terms can vary depending on the arrangement, and there is usually no formal application process. You may agree to pay them back in full by a certain date or make small repayments over time.

- Pros:

- No interest rates or fees.

- Flexible repayment terms and conditions.

- Fast access to cash without a formal approval process.

- Cons:

- Can cause personal strain or tension if repayment is delayed or not made in full.

- There may be an emotional cost if you are unable to repay the loan as agreed.

- The amount you can borrow may be limited by what your friends or family are willing to lend.

8. Cash Advance from a Credit Card

While credit card cash advances are similar to payday loans in that they allow you to borrow money quickly, they offer slightly more flexibility. When you need immediate cash, a credit card cash advance lets you access funds directly from your credit card, either through an ATM withdrawal or a bank. It’s a convenient option for those who have available credit but need fast access to cash for an emergency.

- How It Works: With a cash advance, you can withdraw cash directly from your credit card at an ATM or bank. The loan amount will depend on your available credit and the policies of your credit card issuer. You’ll be charged a fee (usually a percentage of the amount borrowed) and higher interest rates than standard purchases, which often begin accruing immediately.

- Pros:

- Fast access to funds—typically available within hours.

- Easy application process as it requires only the use of your credit card.

- No need for additional paperwork or credit checks if you have an active credit card account.

- Cons:

- High-interest rates—cash advances often carry much higher rates than regular credit card purchases.

- Cash advance fees can be steep, making the loan more expensive.

- There’s no grace period for repayment, meaning interest starts accumulating immediately.

- Low borrowing limits depending on your credit card’s available balance.

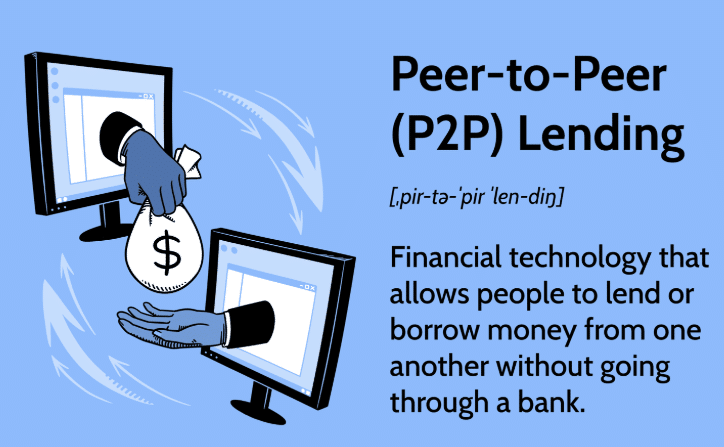

9. Peer-to-Peer (P2P) Loans

Peer-to-peer lending platforms, also known as P2P loans, are an alternative to traditional bank loans. These online platforms allow individuals to borrow money from investors rather than financial institutions. P2P lending is gaining popularity as a flexible and accessible form of emergency funding, particularly for those with less-than-perfect credit histories.

- How It Works: P2P lending platforms, such as LendingClub or Prosper, connect borrowers with individual investors willing to lend money. Borrowers apply online, detailing their financial needs and personal information. Investors then review the applications and choose which borrowers to fund. P2P loans typically offer both secured and unsecured options, depending on the platform and borrower needs.

- Pros:

- Accessible to individuals with less-than-perfect credit scores, especially with platforms that cater to subprime borrowers.

- Flexible repayment terms, often more favorable than those of traditional lenders.

- Competitive interest rates, particularly for borrowers with good credit, and faster approval times than traditional banks.

- Cons:

- As a relatively new lending model, P2P loans may carry more risk due to less regulation.

- While faster than banks, P2P loans may still take a few days to process.

- For large loans, the approval process may be more challenging since investors are individually funding portions of the loan.

- P2P platforms often charge origination fees, which can reduce the amount of funds you receive.

10. Bad Credit Emergency Loans

Bad credit emergency loans are specifically designed for individuals with poor credit histories. If you have a low credit score or have experienced financial challenges in the past, this type of loan can provide emergency funding when other options may not be available. They are typically offered by online lenders and may come with higher interest rates due to the increased risk to the lender.

- How It Works: Many online lenders offer emergency loans specifically for people with bad credit. These loans can be secured (requiring collateral such as a car or home) or unsecured, depending on the lender and loan type. The approval process is generally faster than traditional loans, but the interest rates can be much higher to compensate for the higher risk to the lender.

- Pros:

- Accessible to individuals with poor credit or no credit history.

- Fast approval and funding times.

- Potentially flexible loan terms, with both small and large loan options available.

- Cons:

- High interest rates, which can make the loan significantly more Cost over time.

- Fees for processing and origination may further increase the overall cost.

- Secured loans may require collateral, meaning you could lose assets (e.g., a car or home) if you are unable to repay the loan.

Also Read: What Are Emergency Loans And How Do They Work?

Conclusion

Personal emergency loans can provide essential financial relief in times of crisis, but it’s important to understand the differences between the types available to you. From traditional personal loans to payday loans and even newer alternatives like peer-to-peer lending, each option comes with its own benefits and drawbacks. By carefully assessing your financial situation, credit score, and repayment ability, you can choose the most appropriate loan to meet your immediate needs without jeopardizing your long-term financial health. Be sure to read the fine print of any loan agreement to fully understand the terms, interest rates, and repayment schedules before accepting the loan offer.

FAQS:

1. What is a personal emergency loan?

A personal emergency loan is a type of loan that provides quick access to funds during unexpected situations or financial crises. These loans can help cover urgent expenses such as medical bills, car repairs, home repairs, or other unforeseen costs. Personal emergency loans can be unsecured (no collateral required) or secured (where you offer an asset like your car or home as collateral).

2. How do I qualify for a personal emergency loan?

The qualification criteria for a personal emergency loan vary by lender. Typically, lenders look at your credit score, income, employment status, and debt-to-income ratio. Some lenders may require a credit check, while others, like payday loan lenders, may not. However, having a higher credit score and stable income improves your chances of qualifying for a loan with favorable terms and interest rates.

3. How quickly can I get an emergency loan?

Emergency loans can be disbursed very quickly, often within 24 to 48 hours. However, the exact time it takes depends on the type of loan and the lender. Online lenders and payday loans typically offer faster approval and funding, while traditional banks may take longer to process the loan application and fund the loan.

4. What types of emergency loans are available?

There are several types of emergency loans:

- Traditional personal loans: Typically unsecured, with fixed loan amounts and repayment terms.

- Payday loans: Short-term loans for small amounts, often with high-interest rates.

- Online loans: Loans provided by online lenders with quick approval and funding.

- Credit card cash advances: Borrowing cash against your credit card’s available balance.

- Home equity loans or HELOCs: Loans that use your home as collateral.

- Peer-to-peer (P2P) loans: Loans funded by individual investors via online platforms.

- Bad credit loans: Loans designed for individuals with poor credit histories.

5. Can I get an emergency loan with bad credit?

Yes, there are emergency loan options available for individuals with bad credit. While your credit score may impact the terms of the loan (e.g., higher interest rates or smaller loan amounts), online lenders, payday loans, and certain types of personal loans may be more flexible in approving loans for individuals with less-than-perfect credit.

6. How much can I borrow with a personal emergency loan?

The amount you can borrow with a personal emergency loan depends on the type of loan and the lender. For example:

- Payday loans typically range from $100 to $1,000.

- Traditional personal loans can offer larger amounts, often between $1,000 and $50,000.

- Home equity loans may provide higher amounts based on the value of your property.

- Credit card cash advances are typically limited to your available credit balance. The loan amount will also depend on factors like your income, creditworthiness, and the lender’s policies.

7. What are the risks associated with emergency loans?

While emergency loans can provide quick relief, they come with risks:

- High-interest rates: Some emergency loans, especially payday loans and cash advances, carry high interest, making them expensive.

- Short repayment terms: Many emergency loans require quick repayment, often within weeks or a month, which can be difficult to manage if your financial situation doesn’t improve in that time.

- Debt cycle: If you cannot repay the loan on time, you may end up taking out another loan to cover the previous one, leading to a dangerous cycle of debt.